AI memory: long the bottleneck, skip the blow-off

High-bandwidth memory is a real, sold-out bottleneck, but the trade is not to chase Micron after a near-tenfold run into its highs. I own the bottleneck through Camtek, the cleaner inspection pick-and-shovel, and sell a defined-risk Micron put spread for income. Conviction is medium, rising to high on a pullback fill or a confirming June 24 print.

Semiconductors strategy. High-bandwidth memory, the stacked memory chips that feed artificial-intelligence accelerators, is a real and sold-out bottleneck, but the edge is in the expression, not the headline name. I own it through Camtek, ticker CAMT, the inspection equipment every memory maker depends on, entered as a barbell, and I sell a defined-risk Micron, ticker MU, put spread to harvest the leader's rich premium. I commit a starter today and arm the rest for a wash-out.

| Metric | Detail |

|---|---|

| Recommendation | Own the bottleneck through Camtek (CAMT), entered as a barbell. Sell a Micron (MU) put spread for income. Avoid chasing the leader |

| Conviction | Medium on the structure today; high on the thesis over 18 to 24 months. To high on a pullback fill or a confirming June 24 print |

| Vehicle | CAMT equity in a near-costless collar, a January 2027 MU put spread, and a chip-sector ETF short. Full legs in section 8 |

| Horizon | Equity tail 18 to 24 months; options to January 2027, extendable to 2028 |

| Expected return | Income credit near 30% of the spread width, win rate near 71%; convex equity upside if orders print |

| Reward to risk | Defined on both legs; the income leg risks the spread width net of the credit |

| Carry | Positive: the put spread is sold for a credit, the collar struck near zero cost |

| Maximum loss | Bounded; both legs defined-risk. Modeled tail near 4% of the book after a partial hedge |

1. The bottleneck is real

The structural case is genuine and current, not a forecast. Calendar-2026 high-bandwidth memory is sold out across all three makers, SK Hynix, Samsung, and Micron, increasingly under three-to-five-year contracts. That is a break from the quarterly pricing that has long defined commodity memory. Customers receive only about 50% to 66% of the volume they request.

The mechanism is physical. A bit of high-bandwidth memory consumes roughly three to four times the wafer area of conventional dynamic random-access memory, or DRAM. So the ramp crowds out commodity supply and tightens the whole DRAM market. Bit demand for the product grows more than 70% in 2026, after more than 130% in 2025, pulled by accelerator roadmaps at Nvidia and the hyperscale custom chips.

The cyclical alarms are quiet for now. Supplier inventories sit near two to four weeks, against the more than fifteen weeks that preceded every prior downturn. There is no order hoarding yet. The real risk is timing and peak magnitude, not an imminent glut, and that distinction shapes the entire trade.

2. Why chasing the leader has no edge today

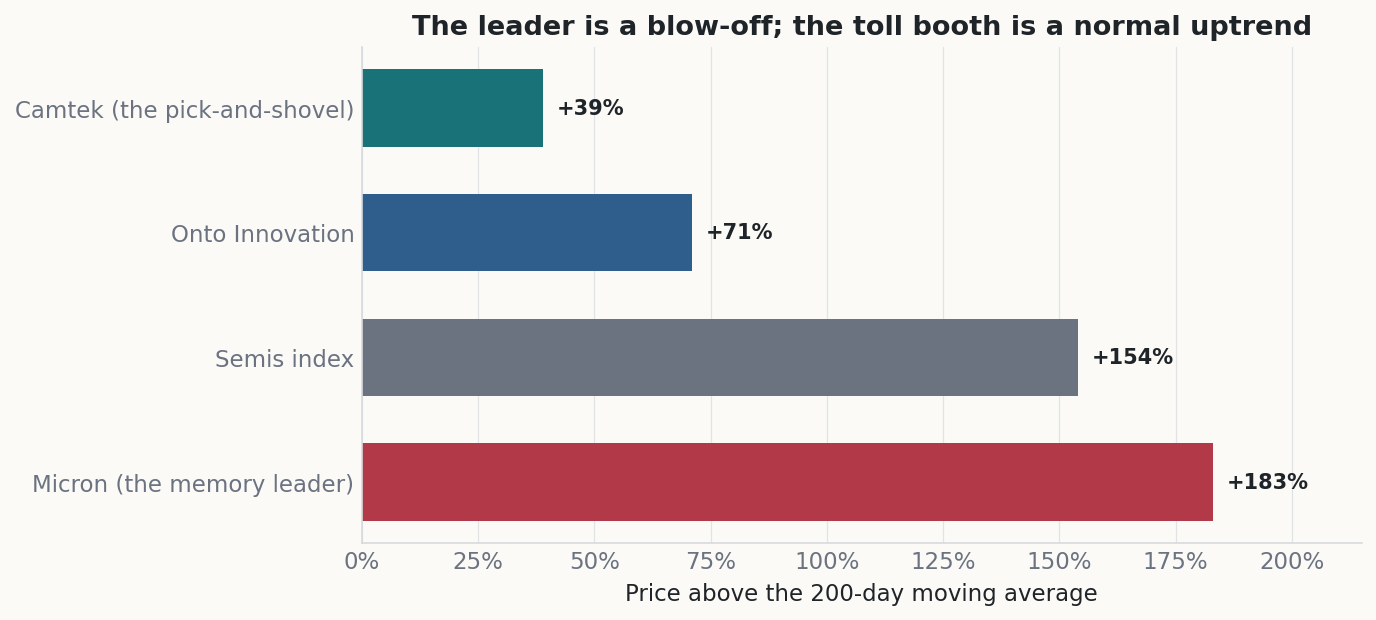

The obvious expression is to buy Micron, the most liquid optionable memory name. That fails on entry and on quality, not on the long-run story. Micron trades at its fifty-two-week high after a near-tenfold twelve-month run, more than 180% above its two-hundred-day moving average (Exhibit 1). The whole memory complex is pinned at highs and crowded.

Exhibit 1. Distance above the two-hundred-day moving average. Micron is a parabolic blow-off pinned at its high; Camtek sits in a normal uptrend, about 6% below its own high.

Two quality points compound the late entry. Micron is the number-three supplier, near 21% share against roughly 60% for SK Hynix, so it is a price-taker in the share war. Its record gross margin, guided near 81%, is largely peak-cycle pricing rather than a permanent level. Realized volatility has accelerated into the blow-off, so the options market charges a steep premium to express any view through Micron. Buying convexity into that premium is a losing proposition before the thesis is even tested.

3. The cleaner expression: the inspection toll booth

If the bottleneck is the constraint, the cleaner exposure is the toll booth, not the most crowded car on the road. Camtek sells the three-dimensional metrology and inspection tools that measure the through-silicon vias and bump stacks inside high-bandwidth memory. It sells to the memory makers, so it is agnostic to which one wins the share war. Its revenue scales with unit and layer-count growth, the structural driver, rather than with memory pricing, the cyclical one.

The entry is far cleaner than the leader's. Camtek sits about 39% above its two-hundred-day moving average and roughly 6% below its high, a normal uptrend rather than a vertical move. Its gross margin near 51% is structurally normal, so it carries little of the peak-pricing air that sits under Micron. Onto Innovation, ticker ONTO, is a close substitute in the same process-control niche, though it sits more extended.

I am candid about the impurity. High-bandwidth memory is not a disclosed revenue line at Camtek. It is roughly 20% to 35% of revenue, bundled inside an artificial-intelligence segment near half of sales that also holds logic and advanced-packaging work. The disclosed order book names two memory customers, not three. So this is a high-quality advanced-packaging proxy, a second-derivative bet on customer capital spending, not a pure-play.

4. What the pick-and-shovel actually is

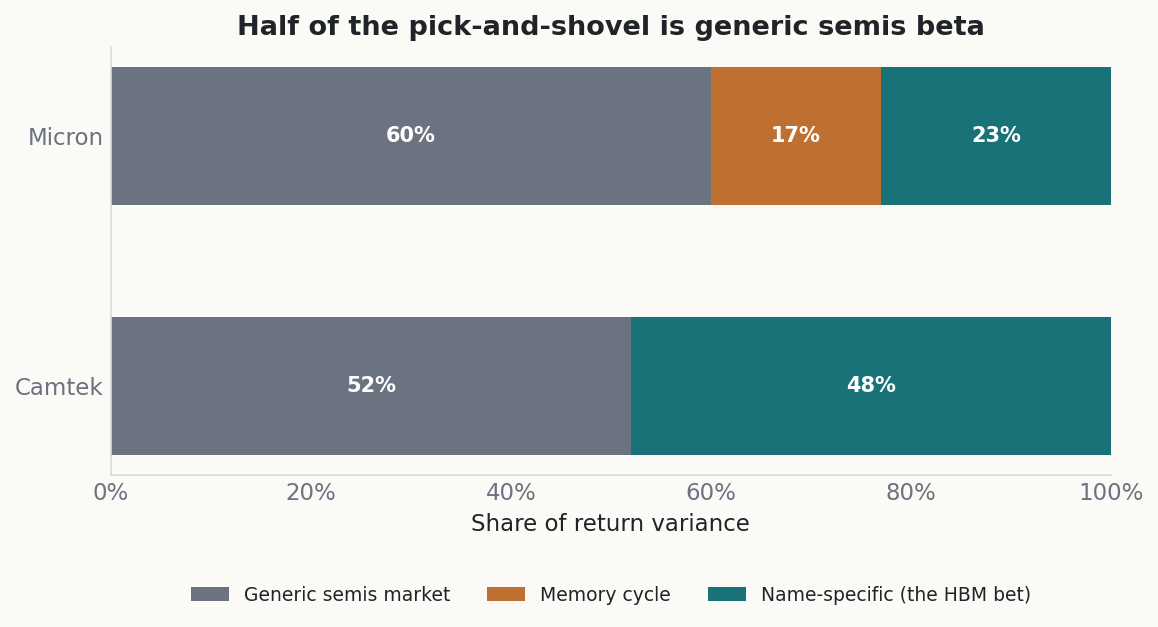

A factor decomposition disciplines the romance of the toll-booth story. I regress each name on three orthogonal factors built from the return history: a broad chip-sector market factor, a memory-cycle factor, and a name-specific residual. For Camtek, 52% of return variance is generic sector beta and 48% is name-specific (Exhibit 2). For Micron, 60% is sector beta and 17% is the memory cycle.

Exhibit 2. Variance share by factor. Roughly half of Camtek's risk is the chip sector you can buy more cheaply through an index. The name-specific slice is the part that carries the high-bandwidth-memory bet.

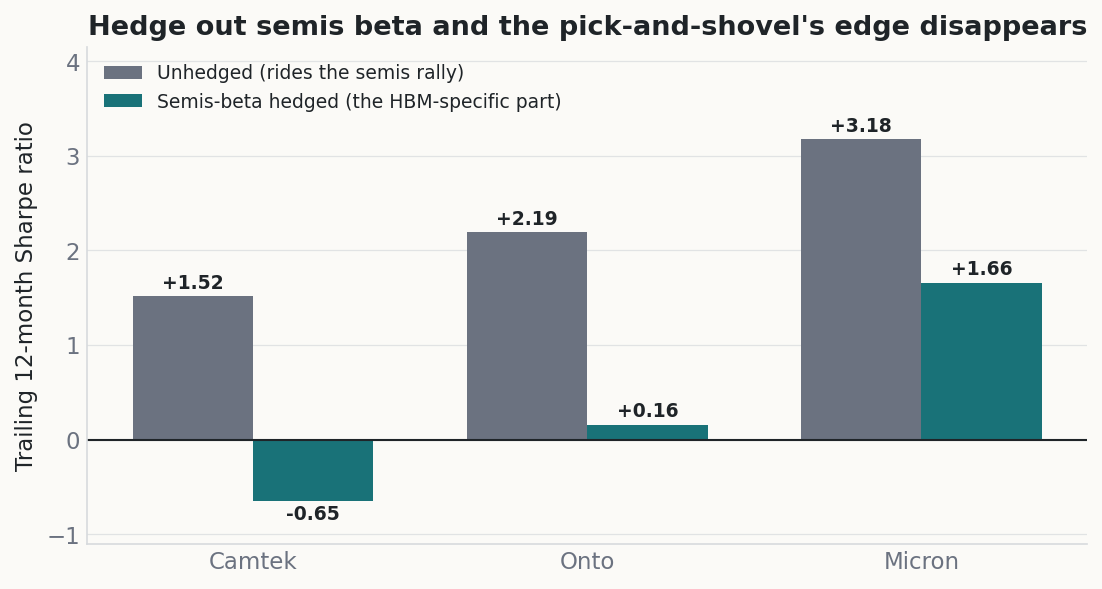

The hedge overlay is the sobering part. If I short the sector index against each long to isolate the name-specific return, Camtek's trailing twelve-month Sharpe ratio falls from plus 1.52 to minus 0.65 (Exhibit 3). Almost all of its move was riding the sector rally. Beta-adjusted, it carried no high-bandwidth-memory alpha yet. Micron, the impure leader, kept positive hedged performance, because the memory cycle was real relative outperformance.

Exhibit 3. Sharpe ratio before and after hedging the sector beta. The pick-and-shovel's edge is mostly sector beta; the thesis is a forward bet on order growth, not a trend already in the price. I size accordingly.

The reading is not that Camtek is a bad vehicle. It is that the bottleneck premium has not yet shown up in its name-specific return, so I treat it as a forward thesis to be entered with discipline, and I size the sector beta as a risk to manage rather than an edge to pay for.

5. The combined book and its hidden tail

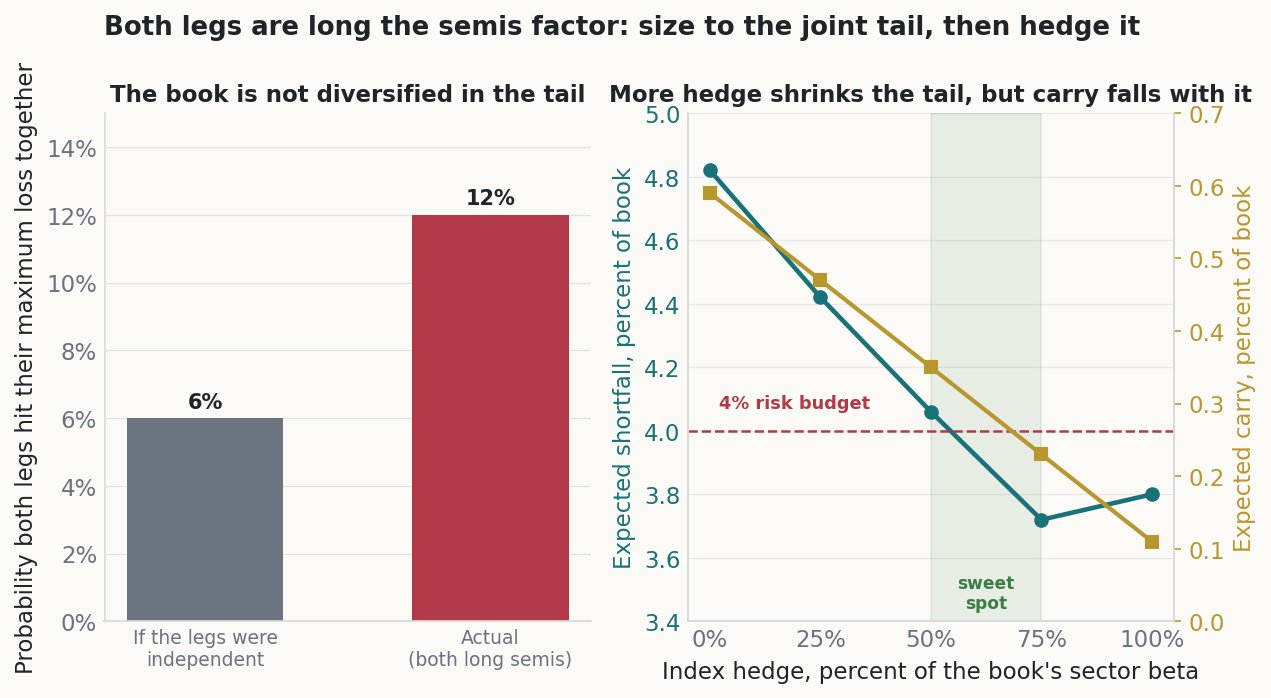

The two legs do not diversify the way a naive view assumes. The Camtek long and the Micron put sale are both long the chip sector, so a sector sell-off pushes against both at once. In a joint simulation the probability that both legs reach their maximum loss together is 12%, against 6% if they were independent, twice the naive figure (Exhibit 4, left). The book is concentrated in the tail, so I size to the joint risk, not to the sum of the parts.

Exhibit 4. Left: both legs share the sector factor, so the joint tail is twice the independent figure. Right: hedging roughly half to three-quarters of the book's sector beta brings expected shortfall to the 4% budget, while carry falls as the hedge rises. Hypothetical and point-in-time.

A modest index hedge fixes the concentration. Shorting a chip-sector exchange-traded fund against the book trims the shared tail. The tradeoff is informative: a hedge of roughly half to two-thirds of the book's sector beta brings the modeled expected shortfall, the average loss across the worst outcomes, to the 4% budget while keeping most of the carry (Exhibit 4, right). A full hedge over-corrects, because the option legs already cap their own upside, so it gives up carry and adds a melt-up cost for little further tail relief. A partial hedge is the sensible point.

6. The entry plan: chase, wait, or barbell

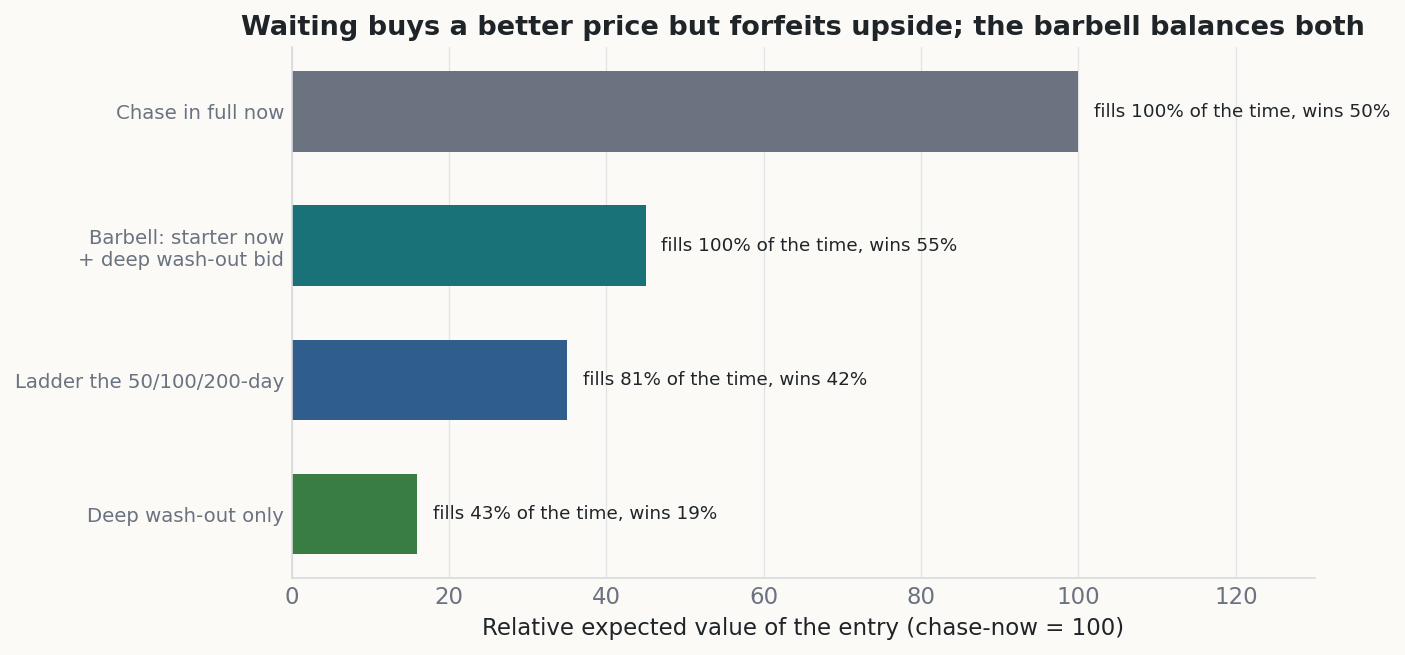

Entry timing is its own decision, and the honest answer is not a slogan. Under a flat-to-higher central path, buying the full position now carries the highest expected value, because waiting forfeits upside on the days the pullback never comes (Exhibit 5). Waiting buys a better price and a margin of safety, but it fills only part of the time. The barbell resolves the tension.

Exhibit 5. Relative expected value of four entry tactics, with fill probability and win rate. Waiting in full forfeits upside; the barbell, a starter now plus a deep wash-out bid, keeps full deployment and still improves the average price.

I therefore commit a starter today and rest limit bids into the dips. A pullback to the fifty-day line, about 8% below spot, has about an 81% chance of printing over the tactical window; the hundred-day, about 13% below, about 70% likely, and the two-hundred-day, about 28% below, about 43%. The barbell holds full deployment with the highest win rate of the laddered tactics, and a wash-out improves my blended entry without my forfeiting the upside if it never comes.

7. The income leg: harvest the leader's volatility

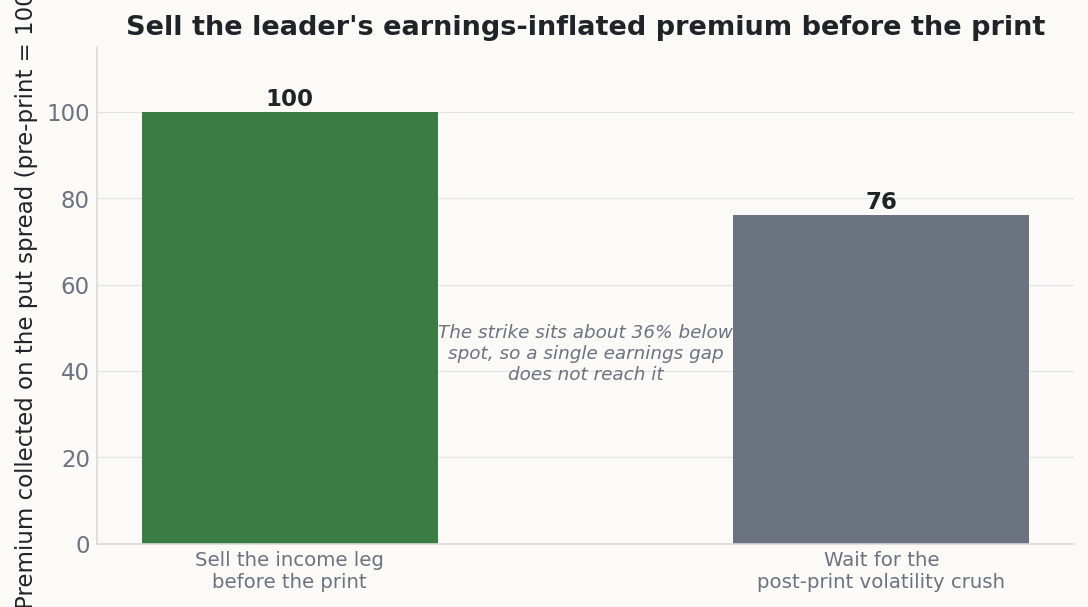

The same blow-off that makes Micron a poor outright long makes it a rich premium to sell. Rather than pay the steep implied volatility for Micron upside, I sell a January 2027 put spread struck deep below spot (legs 4 and 5 in section 8). The credit is near 30% of the spread width, with a modeled win rate near 71%. If the short strike is ever assigned, I own Micron near 40% below today's price, net of the credit, a wash-out I would want, with the loss defined by the long wing.

The timing of the sale matters. Micron reports fiscal third-quarter earnings on June 24, and the print inflates the premium. Selling before the report captures roughly a quarter more credit than waiting for the post-print volatility crush (Exhibit 6). The short strike sits about 36% below spot, far enough that a single earnings gap does not reach it, so I collect the inflated premium without wearing undue gap risk on the binary.

Exhibit 6. Premium on the put spread, before the earnings print versus after the volatility crush. The seller of premium wants to act before the print; the deep strike survives a single earnings gap.

The protective leg on the equity is close to free. A Camtek collar, a long stock position wrapped with a downside put financed by selling an upside call, prices near zero net cost in the January 2027 tenor. So I cap the equipment-cyclical downside without paying away the carry. The January 2027 tenor gives the most credit per year; the January 2028 tenor terms the position across the 2027 capacity window for a reader who wants the longer protection.

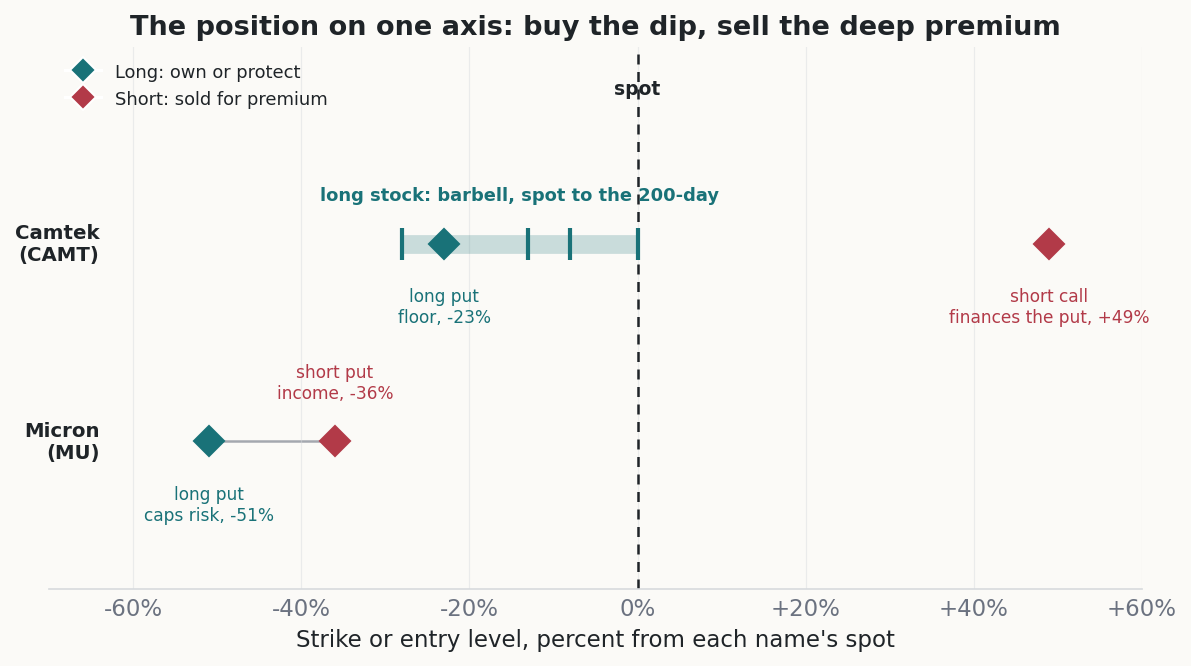

8. The assembled position

Pulled together, the trade is five legs across two names plus a sector-hedge overlay, and it reads as one position: long the bottleneck through the toll booth, paid to wait through the leader's premium, and defined-risk on each wing. Legs 2 to 5 are January 2027 options, and the equity tail runs 18 to 24 months. The ledger lists every leg:

| # | Leg | Level | Role |

|---|---|---|---|

| 1 | Long CAMT stock, barbell | Spot to 28% below | Core long |

| 2 | Long CAMT put | 23% below | Downside floor |

| 3 | Short CAMT call | 49% above | Finances the put |

| 4 | Short MU put | 36% below | Income, dip entry |

| 5 | Long MU put | 51% below | Risk cap |

| 6 | Short chip-sector ETF | 50% to 67% of beta | Tail hedge |

On a single axis scaled to each name's spot, the shape is plain (Exhibit 7). The Camtek legs bracket a long stock position bought on the dips, floored by the put and capped by the financing call. The Micron legs sit far below spot, where I am paid to supply the downside that the blow-off has made expensive.

Exhibit 7. Every leg on one axis, in percent from each name's spot. Long legs (own or protect) in teal, short legs (sold for premium) in red. The Camtek collar brackets the stock; the Micron put spread sits deep below, where the premium is richest.

9. Construction and sizing

The sizing follows the joint-tail work, not the marginal legs. I size the combined Camtek collar and Micron put spread together, apply a partial sector hedge, near half to two-thirds of the book's sector beta, and hold the modeled expected shortfall near the 4% budget. Both legs are defined-risk, so the maximum loss is bounded by the collar width plus the put-spread width net of credits, before the hedge offsets part of the shared tail.

The carry is positive while I wait. The Micron put spread is sold for a credit, the Camtek collar is struck near zero cost, and the equity pays no option decay against me. The starter equity is a fraction of the full target, with the remainder armed as limit bids into the trend supports. A buy-limit, never a buy-stop, fills at or below my price on a gap.

10. The conviction clock

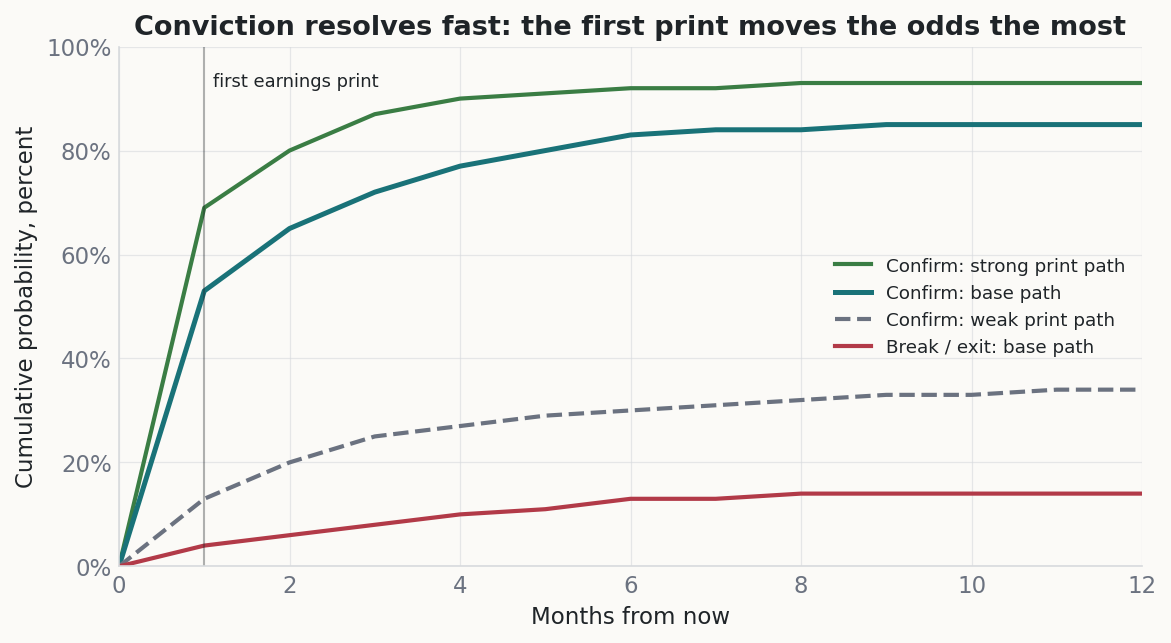

Conviction here is a function of data, not a calendar. I model two competing monthly hazards: confirmation, which raises conviction toward a full position, and a break, which retires the income leg. The calendar is front-loaded. The June 24 Micron print alone resolves more than half of the confirmation odds in the first month (Exhibit 8).

Exhibit 8. Modeled cumulative probability of confirmation against a break, by scenario. The first print moves the odds the most, so I add on confirmation and retire the income leg on a break. A framework, not a forecast.

The signals are concrete. Confirmation is a gross margin near 81% holding or rising, a reaffirmed sold-out position, on-schedule next-generation qualification, and firm contract prices. A break is margin compression, softening sold-out language, sequential price declines spreading from the current generation, or an equipment-order air-pocket. I add the armed equity on confirmation and stand down the premium sale on a break.

11. Catalysts and timeline

The near path is dense. Micron reports on June 24, the first and highest-signal event. Samsung and SK Hynix report in late July, the independent supplier-side reads. Through the second half of 2026 the next-generation accelerator ramp pulls memory demand, and the independent contract-price trackers print on a monthly-to-quarterly cadence.

The lower-frequency tests run further out. The 2027 capacity additions, synchronized mega-fab volume and yield ramps across all three makers, are the seed of the next oversupply, and I monitor them as a risk rather than a base case. The hard checkpoint is the turn in supplier inventories and contract prices. If inventories build past prior-cycle thresholds and prices roll sequentially, the cycle is turning, and I retire the income leg and trim the equity.

12. Risks and invalidation

The first risk is the cycle itself. Memory peaks are brutal, with prior episodes giving back half the equity value and swinging gross margins from records to losses. My defense is structural: defined-risk legs, a deep income strike, a half sector hedge, and a conditional equity entry rather than a chase. A sector-wide sell-off remains the dominant tail, because both legs lean long the chip sector.

The name-specific risks are concrete. Camtek's exposure is a second-derivative bet on customer capital spending, and equipment orders are lumpy and weighted to the back half, so the name can disappoint on timing even with the thesis intact. Its high-bandwidth-memory exposure is overstated by the headline, near 20% to 35% of revenue, so a pure-play reader is buying advanced packaging. Invalidation is a confirmed inventory build with sequential contract-price declines, or a Camtek order air-pocket, at which point I exit the income leg and trim to the residual starter.

13. The bear case in plain terms

I hold the other side honestly. The bottleneck is real but consensus, and the move is largely in the price: the leader has advanced near tenfold and the complex is crowded at its highs. The cleaner-looking pick-and-shovel is half sector beta, and beta-adjusted it has shown no name-specific edge yet, so the thesis is a forward bet rather than a trend in motion. Record margins are peak-cycle pricing, and synchronized capacity lands in 2027.

That is why I refuse the chase and accept a medium conviction today. The structural case supports exposure; the price action demands structure and patience. I own the bottleneck through the toll booth and a starter, get paid to wait through the premium sale, define the risk on both legs, and let the data raise or retire the position. The disciplined posture earns carry now and converts to conviction on a pullback fill or a confirming print.

Disclosures

This document is produced for informational purposes only. It is not investment advice, nor an offer or solicitation to buy or sell any security or derivative. The analysis reflects my views as of June 22, 2026 and is subject to change without notice. Figures are drawn from a point-in-time research snapshot and are expressed in relative terms, and they have not been updated for subsequent market moves. The scenario, factor, and simulation analyses are hypothetical, are based on modeled assumptions, and are not a forecast or a guarantee of future results. Options carry the risk of total loss of premium, a short put spread can lose the full width net of the credit received, and equipment and memory equities can produce outsized losses in a gap. I may hold positions in the securities referenced. Readers should perform their own due diligence and consult a licensed adviser before acting.

Sources used: Micron Technology investor relations, SK Hynix newsroom, Samsung Semiconductor, TrendForce market research, Camtek investor relations, Onto Innovation investor relations, Nvidia newsroom, Counterpoint Research, Reuters technology coverage.