SpaceX after the listing: relative value over direction

SpaceX listed on June 12, 2026 under the ticker SPCX, and it is the hottest new name on the market. The obvious ways to play it are already in the price. The clean expression is relative value: a bullish Rocket Lab call spread against a bearish Destiny Tech100 put spread, both defined risk. A simulation calibrated to current realized volatility gives the pair a small positive expected value and a 77% win rate, with risk capped at the debit. I hold no directional SPCX position. The leveraged exchange-traded fund short that looks like a free decay harvest is negative expected value once borrow is paid, so I express any bearish view through defined-risk puts instead.

Equity event strategy. SpaceX listed on June 12, 2026 under the ticker SPCX, and it is the most crowded new name on the tape. I recommend no directional position in the stock. The clean trade is relative value: long a Rocket Lab call spread against a bearish Destiny Tech100 put spread, both defined risk. A simulation calibrated to current realized volatility gives the pair a small positive expected value, a 77% win rate, and a loss capped at the debit. I also avoid the obvious directional alternative, a short in a leveraged exchange-traded fund, which wins often but loses money on average.

| Metric | Detail |

|---|---|

| Recommendation | Initiate the defined-risk pair, small. No directional SPCX position |

| Conviction | Medium. The pair carries a small positive expected value while Destiny Tech100 realized volatility exceeds implied |

| Vehicle | Long a Rocket Lab, ticker RKLB, 110 to 130 call spread against a Destiny Tech100, ticker DXYZ, 30 to 25 put spread, ratio 1 to 4, both August 21, 2026 |

| Horizon | To August 21, 2026 |

| Day-one committed capital | 1,866 dollars per unit. I size 2 to 5 units, about 0.4 to 0.9% of the account |

| Expected return | Small and positive. Mean near plus 4% of the debit, median near plus 7%, with a 77% win rate |

| Reward to risk | Capped. Maximum gain 2,134 dollars against maximum loss 1,866 dollars per unit. The edge is the positive mean, not a large payout |

| Carry | Slightly negative time value. No borrow, no roll |

| Maximum loss | Bounded at the debit, 1,866 dollars per unit |

1. A reflexive listing that already faded

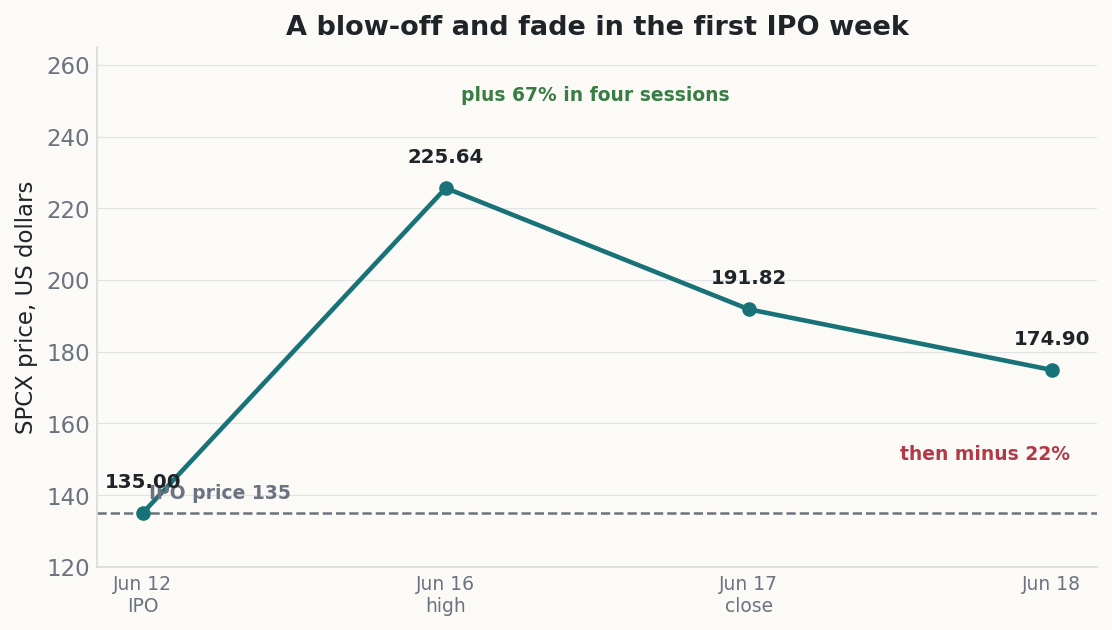

SPCX listed at 135 dollars on June 12. It ran to 225.64 on June 16, then fell to 174.90 by June 18 (Exhibit 1). That path is a blow-off, not a re-rating. The free float is about 4.3% of shares, so modest order flow moves the price. Dealers hedging heavy call demand into a near-empty book set the level, not valuation.

Exhibit 1. SPCX in its first week, from a point-in-time snapshot. The listing ran 67% above its issue price in four sessions, then gave back most of the move. Reflexive flow into a tiny float set the level.

The company is genuine and dominant. Starlink, its satellite-internet unit, earned 11.4 billion dollars of revenue and 4.4 billion dollars of operating profit. At about 2 trillion dollars the equity trades near 100 times sales. A great business can still be a crowded price.

2. Why the obvious trades have no edge

Three direct expressions look tempting, and each fails on its own terms. Buying the stock chases a name up 30% from issue and down 22% from its high in a single week. Selling options looks rich at 155% to 167% implied volatility, the market price of expected movement, but realized volatility runs above 200%. On that gap the options are not expensive, so a short-volatility trade is underpaid.

Buying volatility pays the same gap but bleeds if the move calms. The listed chain opened on June 16 with one monthly expiry and thin open interest. A clean, fillable options structure on the single name does not yet exist. The edge sits in the relative value around SPCX, not in a SPCX line item.

3. The proxy premium has already collapsed

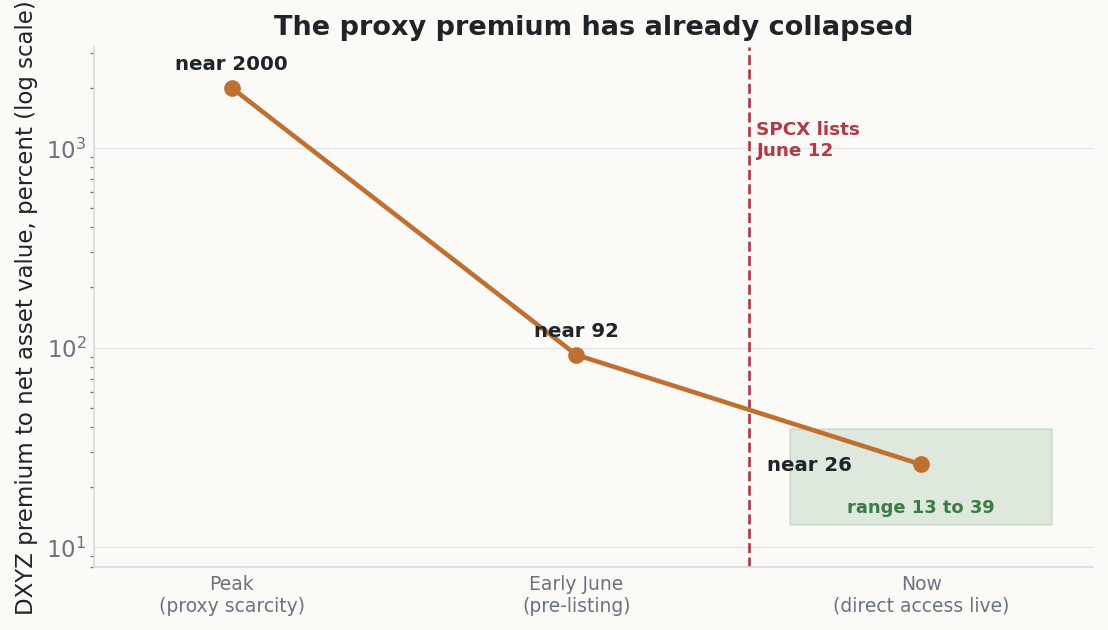

Destiny Tech100, ticker DXYZ, is a closed-end fund that holds SpaceX at about 16% of assets. Before the listing it traded far above its net asset value, the per-share worth of its holdings, because retail had no other route in. That premium reached roughly 2000% at the extreme and about 92% in early June. Direct access arrived on June 12, and the premium fell toward a 13% to 39% range (Exhibit 2).

Exhibit 2. The DXYZ premium to net asset value, from a point-in-time snapshot. Direct access to SpaceX removed the reason for the premium, and most of the collapse is behind us. The current reading is a range because the published net asset value is dated March 31.

The exact figure is uncertain, since the last reported net asset value is dated March 31. The direction is not uncertain. The reason for the premium has gone. A 1 billion dollar at-the-market program keeps issuing DXYZ stock above net asset value, which caps the premium further. I want to be short that decay, with defined risk.

4. Why I express the view as a pair

I pair the rich proxy short against a long operator. Rocket Lab, ticker RKLB, is a listed launch and space-systems company with 601.8 million dollars of revenue and a 2.2 billion dollar backlog. A well-funded public SpaceX validates the sector and lifts launch demand. Rocket Lab does not compete with Starlink in direct-to-phone service, so it carries the theme without the head-to-head risk.

Rocket Lab also joins the Nasdaq-100 index on June 22, which forces index funds to buy. I hold the proxy short through a put spread, not a stock short, because DXYZ borrow costs more than 100% a year. Both legs are bought for a debit. Neither can lose more than its premium.

5. The recommended structure

The trade is two defined-risk option spreads, both expiring August 21, 2026, in a 1 to 4 ratio per unit:

- Long 1 Rocket Lab 110 to 130 call spread, at a debit near 6.46 dollars.

- Long 4 Destiny Tech100 30 to 25 put spreads, at a debit near 3.05 dollars each.

One unit costs about 1,866 dollars, and that debit is the entire risk. I size 2 to 5 units, roughly 0.4 to 0.9% of a 1,000,000 dollar account. The Destiny strikes matter. The fund lists no 27.5 strike, so I use the 30 and 25 puts, which sit closer to the 27.80 spot and lift the win rate. Before sending the order I confirm a real two-sided market on the 25 put, because deep out-of-the-money fund puts can quote wide.

6. What the simulation shows

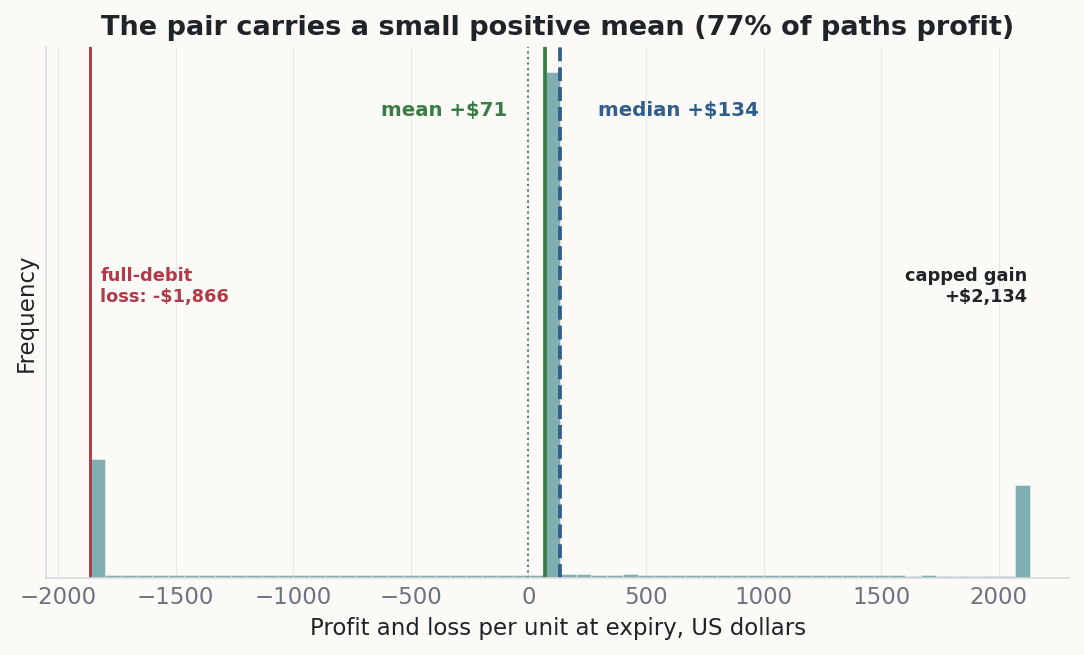

I model the pair with a Monte Carlo simulation, hundreds of thousands of price paths drawn from current realized volatility (Exhibit 3). The result is a small positive expected value, near 71 dollars per unit, with a median near 134 dollars and a 77% win rate. The maximum loss is the 1,866 dollar debit, in every path.

Exhibit 3. Simulated profit and loss of the pair per unit, from a point-in-time snapshot, on a 1,866 dollar debit. The distribution is three-valued: about one path in five loses the full debit, the bulk cluster in a small profit, and a thin tail reaches the 2,134 dollar capped gain. The mean is small and positive.

The edge is modest, and it is honest about its source. The Destiny put spread pays because the fund realizes about 170% volatility against a lower implied volatility, and because its premium reverts toward net asset value. The Rocket Lab call spread, struck on a name that realizes about 105%, adds upside if the sector re-rates. Both legs are bounded, so no path loses more than the debit.

7. Construction and sizing

I size the pair at 2 to 5 units, about 0.4 to 0.9% of the account, where one unit of 1,866 dollars is the debit and the maximum loss. I cap the whole SpaceX theme at 1% of the account. Both legs are bought, so there is no borrow, no margin call, and no forced cover.

Carry is slightly negative, since long options shed time value, but there is no roll cost. I work each spread as a single net-debit order at the mid price. I do not leg the out-of-the-money strikes, because the thin wings can fill at a poor price.

8. The calendar, and why I stand down on direction

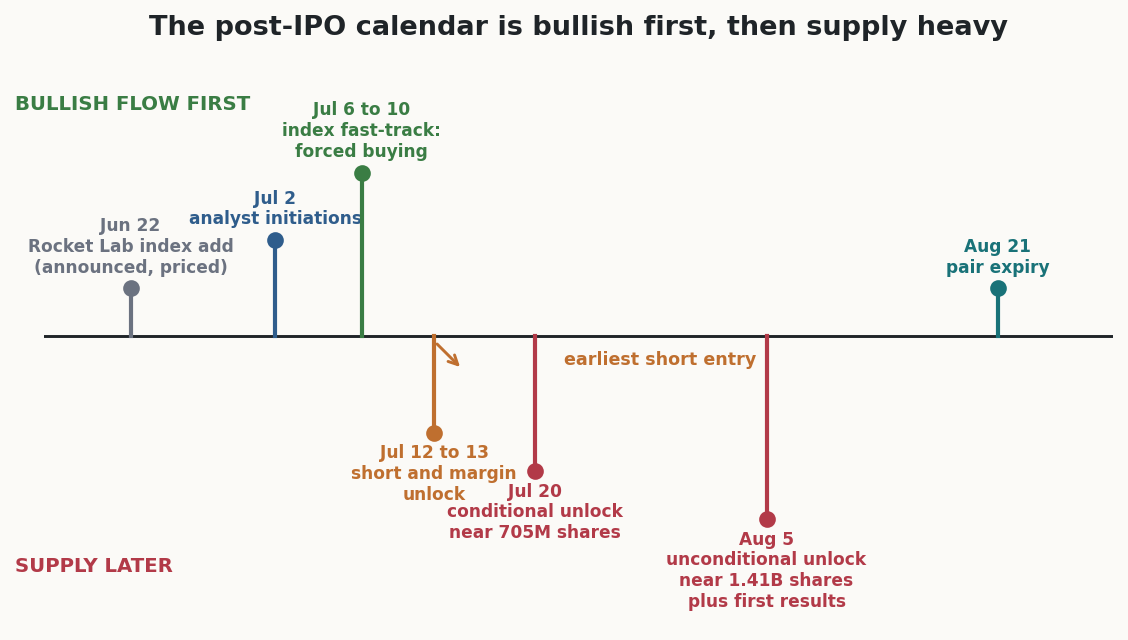

A directional SPCX bet is the dramatic trade, and the lower-conviction one. The post-listing calendar is bullish first, then heavy with supply (Exhibit 4). Two forced-buyer events come first: an analyst initiation wave near July 2, then a possible index fast-track near July 6 to 10 that could force 6.6 to 9.8 billion dollars of buying into a tiny float.

Exhibit 4. The post-listing calendar, from a point-in-time snapshot. Forced buying lands before the trading unlock. The large supply lands on August 5. A bearish bet fights the flow until mid-July, which is why I wait.

The shares cannot be shorted or margined for thirty days, so there is no seller of last resort until about July 12. The bearish supply arrives after that. A conditional release near 705 million shares falls due on July 20. An unconditional release near 1.41 billion shares, about 2.5 times the float, falls due on August 5 with the first results. A bearish bet fights the flow before mid-July and pays only after it, so I hold no SPCX directional position today.

9. Why I avoid the leveraged-ETF short

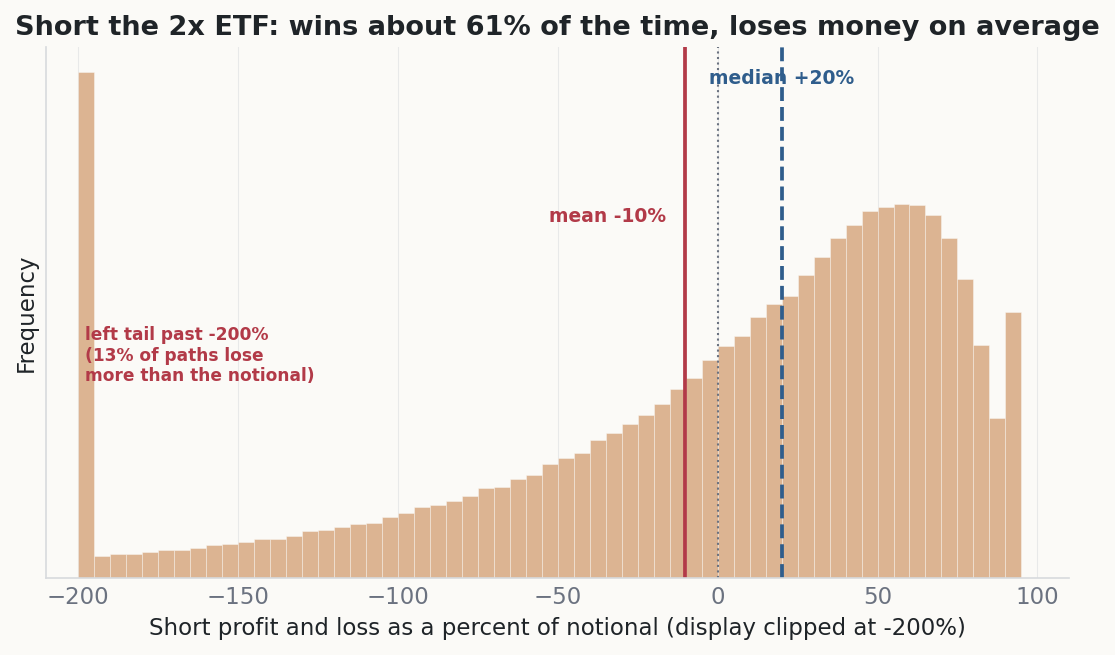

A bearish SPCX view has a tempting expression: short SPCH, an exchange-traded fund that delivers two times the daily SPCX move. The story is that the daily reset bleeds the fund, so the short harvests decay. A simulation does not support the story (Exhibit 5).

Exhibit 5. Simulated profit and loss of the leveraged-fund short, from a point-in-time snapshot, over a three-week hold at 150% annual borrow. The short wins about 61% of the time with a positive median, but the mean is negative and a fat left tail loses more than the notional in a squeeze.

The decay is a median effect, not expected value. With zero-drift daily moves the fund's expected change is about zero, so there is nothing to harvest in the mean. The short wins about 61% of the time, with a median near plus 20%, which is what makes it tempting. But the mean is about minus 10% over a three-week hold, because borrow on a hard-to-borrow fund costs more than any decay, and about one path in eight loses more than the whole notional in a sustained squeeze. It is a coin that pays small and bills large.

So I do not short the fund. If I want SPCX downside after the July 12 trading unlock, I buy defined-risk puts, where the loss is the premium and no borrow or gap can exceed it.

10. The triggers that raise conviction

My conviction on the proxy short rises on three signals. The first is a fresh net asset value mark that confirms a double-digit premium still remains. The second is continued issuance under the at-the-market program, which mechanically caps the premium. The third is the July 12 trading unlock, after which arbitrage can press the proxy directly.

A separate bearish SPCX expression waits on the calendar. The July 12 trading unlock and the August 5 supply are the windows, and I would take them with defined-risk puts, not a leveraged-fund short. Today I hold only the pair.

11. Risks and invalidation

The pair carries three honest risks. A melt-up can re-inflate the DXYZ premium on fresh retail demand, which works against the put spread. Rocket Lab can fade after its index add, since the event is announced and partly in the price. A rising net asset value, from new SpaceX marks, can lift DXYZ even as the premium narrows.

The exits are mechanical. I close the DXYZ leg if a fresh mark shows the premium already near zero. I close the Rocket Lab leg if it breaks below the long strike on weak fundamentals. The hard floor on the whole trade is the debit, which no path can exceed.

12. The bear case in plain terms

I hold the other side honestly. The expected value is small, near 4% of the debit, so the edge is thin and rests on Destiny volatility staying rich to implied. About one path in five loses the entire debit. The name I am long carries a catalyst the market saw coming, and a melt-up can re-inflate the Destiny premium against my put.

The leveraged-fund short, the obvious bearish trade, wins most of the time but loses on average and can gap past its notional. SpaceX is a profitable, dominant asset, and an expensive name can stay expensive. The disciplined position is the small, capped pair, with a positive but modest mean, and defined-risk puts if I want downside later.

Disclosures

This document is produced for informational purposes only. It is not investment advice, nor an offer or solicitation to buy or sell any security or derivative. The analysis reflects my views as of June 19, 2026 and is subject to change without notice. Figures are drawn from a point-in-time research snapshot and have not been updated for subsequent market moves. The scenario analysis is hypothetical and is not a forecast or a guarantee of future results. Options carry the risk of total loss of premium, and a short position in a leveraged fund can produce losses beyond the initial estimate in a gap. Several inputs, including the closed-end fund net asset value and the borrow cost on the leveraged fund, require confirmation at a live terminal before any order. I may hold positions in the securities referenced. Readers should perform their own due diligence and consult a licensed adviser before acting.

Sources used: Nasdaq SPCX listing, U.S. Securities and Exchange Commission EDGAR, Destiny Tech100 investor materials, Rocket Lab investor relations, Nasdaq-100 index methodology, Cboe options data, Morningstar Destiny Tech100 analysis, Reuters markets coverage.