Value over software: a market-neutral rotation

I initiate a market-neutral relative-value position for a higher-for-longer rate regime: long a relative-strength-confirmed quality-value basket (SCHD, XLP, IHF) against long-duration software longs (PLTR, ORCL, WCLD) expressed through defined-risk put spreads. The position is beta-neutral, carries positively, and bounds its downside to the option premium. Conviction is medium today and rises to high on a growth-deceleration signal.

U.S. equity strategy. I recommend initiating a market-neutral relative-value rotation that is long short-duration quality value and short expensive long-duration software. The thesis is that a higher-for-longer rate regime continues to compress long-duration equity multiples while rewarding low-duration cash flows. I size the book to neutral beta so the return reflects the value-minus-duration spread rather than market direction, express the short through defined-risk put spreads to bound the downside, and gate the full position on a growth-deceleration signal that is not yet present.

| Metric | Detail |

|---|---|

| Recommendation | Initiate at half weight; scale to full weight on a growth-deceleration signal |

| Conviction | Medium, rising to high on a growth-deceleration signal |

| Horizon | 3 to 6 months |

| Net beta | Approximately 0.0 |

| Expected return, base case | +4% to +9% of net asset value (NAV) |

| Scenario range | Bounded loss of 3% to 5% to a gain of 8% to 14% of NAV |

| Reward to risk | Above 2.5 to 1, with downside capped by option premium |

| Net carry | +1.4% to +2.0% per annum |

| Maximum loss | Approximately 2% of NAV (defined by premium at risk) |

1. Investment thesis

My thesis rests on a single, testable claim: with the policy rate held high and the next move biased toward a hike, the discount rate facing long-duration cash flows stays elevated, which favors short-duration value over expensive software. The June 17 Federal Open Market Committee (FOMC) meeting removed 2026 cuts and raised the median rate projection to 3.8%, and the 10-year real yield sits at 2.19%. I express the view as a spread rather than a directional bet, because the relative-value relationship is what the macro supports, and because a directional defensive position would lose on its own market exposure in the risk-off scenario the thesis contemplates.

2. Why construction is the edge

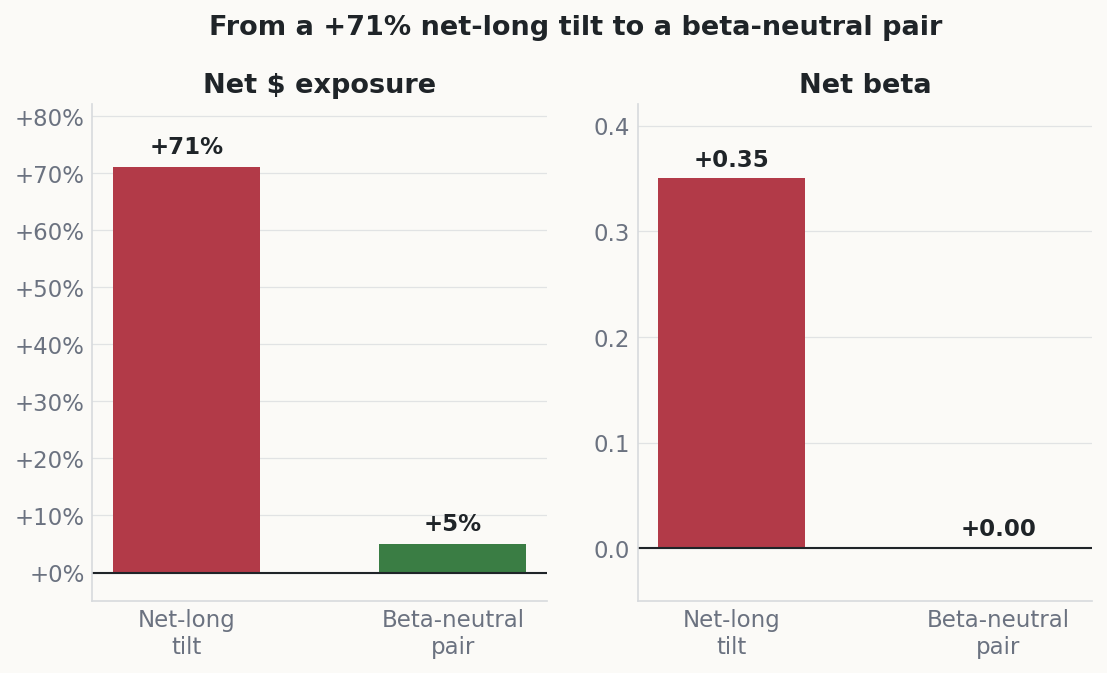

The obvious way to express this view underperforms on construction, not direction. A long basket of XLV, XLP, and XLF against a 29% short in the iShares Expanded Tech-Software ETF (IGV) carries +71% net dollar exposure and roughly +0.35 net beta. That is a net-long position with a partial hedge, and its return is dominated by market direction rather than the rotation. The sign is also adverse: the catalyst is a risk-off rate shock, the scenario in which the broad market falls, yet the book is net long. I address each defect below.

| The obvious long/short | My construction |

|---|---|

| +71% net dollar, +0.35 net beta | Beta-neutral, net dollar near flat |

| Net long into a risk-off catalyst | Slight net-short tilt, leaning into the rate view |

| Short IGV, the consensus short already de-rated below the S&P 500 multiple | Short the over-owned, low-short-interest longs instead |

| Long legs with no relative strength (XLV, XLF, XLP all lagged) | Long only relative-strength-confirmed legs |

| Cash short with borrow cost and squeeze risk | Defined-risk put spreads: no borrow, bounded loss |

3. Trade construction

Long leg

The long leg holds the segments of the value and defensive complex that are outperforming, each confirmed on both a year-to-date and a trailing-month basis:

| Position | Weight | Role |

|---|---|---|

| SCHD | 40% | Schwab U.S. Dividend Equity ETF. Relative-strength (RS) core: up 20% year to date against the S&P 500 at 9.6%, a 3.2% yield, a price/earnings ratio near 18. I trim the 16.5% energy sleeve so the residual exposure is duration and value rather than oil |

| XLP | 30% | Consumer Staples Select Sector SPDR. The lowest-duration, defensive anchor; RS is inflecting (Costco May sales rose 14.5%), with a 2.62% yield |

| IHF | 30% | iShares U.S. Healthcare Providers ETF. The one healthcare expression with RS, on the UnitedHealth earnings-revision inflection. It replaces dead-money XLV. Beta is higher and 41% of assets sit in UnitedHealth and CVS, so it is the first leg I trim if RS fades |

Short leg

The short leg is the decisive part of the construction. Rather than join the crowded software short, I fade the crowded longs in long-duration software, where multiples are extreme and short interest is minimal, and I express the short through defined-risk put spreads:

| Position | Risk budget | Role |

|---|---|---|

| PLTR | 30% | Core short. Palantir trades near 58 times trailing sales, the one still-extreme multiple in the group, with short interest (SI) at 2.25% of float and roughly one day to cover. August earnings is a dated single-name catalyst |

| ORCL | 25% | Secondary short. Oracle is over-owned, with SI near 1.2%. The leg works through the discount-rate and multiple-compression channel, not demand: cloud revenue is accelerating and remaining performance obligations rose 363%. I size it smaller for that reason |

| WCLD | 20% | Composition tail. The fund is equal-weighted and tilts away from the AI megacaps toward decelerating mid-cap software. The put-spread expression sidesteps its thin $250M asset base and scarce borrow |

I exclude three categories as shorts: the consensus software short (IGV), the AI-infrastructure winners (the Vanguard Growth ETF, VUG, holds roughly 46% in them), and the names the market is already short (CRM, NOW, and WDAY carry SI of 7.5%, 5.9%, and 13.6% of float).

4. Portfolio characteristics

The construction converts a directional position into a spread. The cash long leg blends to a beta near 0.72 (SCHD near 0.70, XLP near 0.52, IHF near 0.95). I size the short by delta rather than notional, setting the put-spread delta-equivalent short beta near 0.72 times the long notional. Net beta lands near 0.0, with a small net-short tilt that leans into the rate view. The residual exposure is the spread I intend to own: long short-duration dividend-quality, short long-duration growth software, a dispersion that returned roughly 22 to 28 points in the 2022 rate shock. Because the short is expressed in options, the squeeze tail is capped at the premium rather than at a discretionary stop. I re-hedge the delta weekly, since option gamma drifts the net beta.

Exhibit 1. Net dollar exposure and net beta, a net-long version versus a beta-neutral construction. The beta-neutral build removes the directional market exposure and isolates the value-minus-duration spread.

5. Relative strength

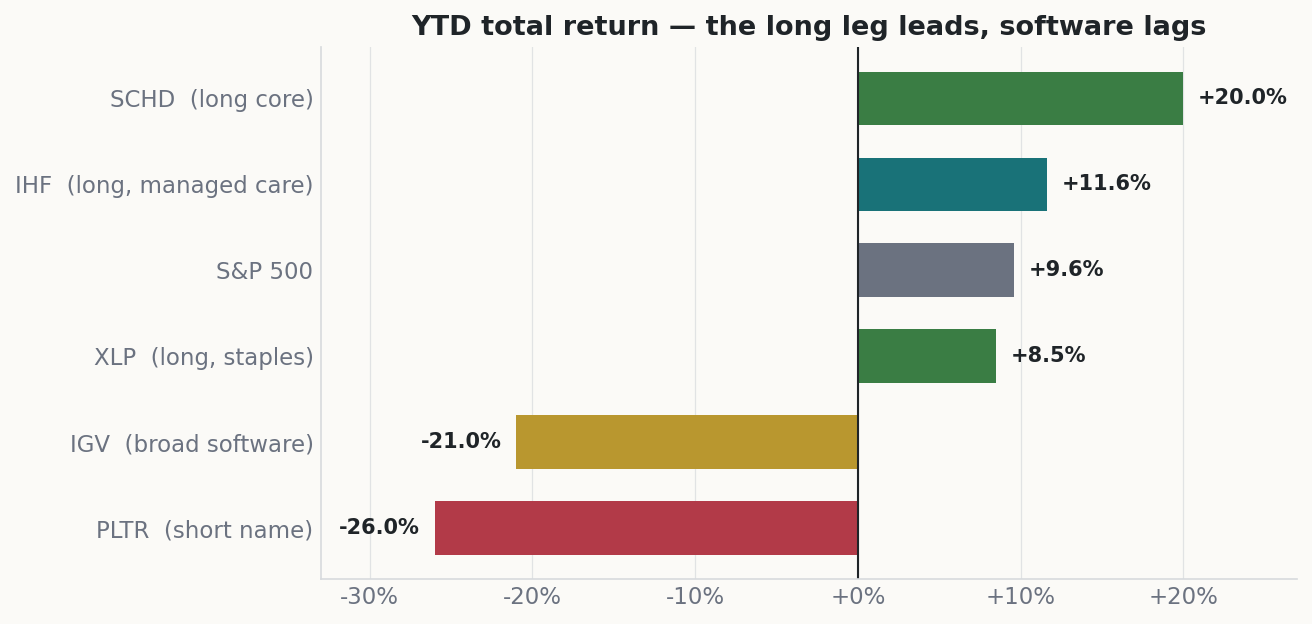

Every position in the long leg carries relative strength, which the broad defensive sectors do not. SCHD is up 20% year to date against the S&P 500 at 9.6%, and up 2.75% over the trailing month against the SPDR S&P 500 ETF at 1.75%. XLP is up roughly 8.5% and inflecting. IHF is up 11.6% and has printed a fresh one-year high. By contrast, the broad defensive sectors (XLV, XLF, XLP) were flat-to-down over the same window, which is why I anchor on the names above instead (Exhibit 2).

Exhibit 2. Year-to-date total return for the long legs, the S&P 500, broad software, and the core short. The long legs lead the index; software lags.

6. Positioning and valuation

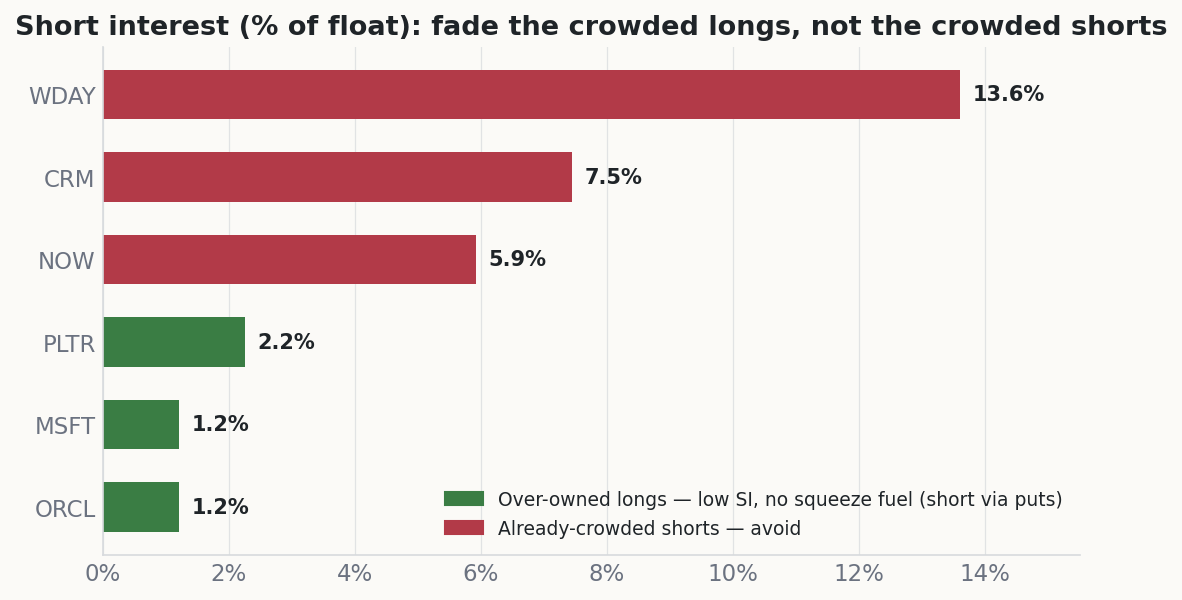

Positioning supplies the edge that direction alone does not. Broad software is the consensus short: hedge funds are net short, roughly $24B was harvested in 2026, and IGV is down 21% year to date and 30% off its peak. Shorting that cohort means leaning into a crowded short against names that are beating and raising. The crowded longs run the other way. Palantir, Oracle, and Microsoft are over-owned with short interest of 2.25%, 1.2%, and 1.2% of float, which is the cohort I fade. The high-short-interest names (WDAY at 13.6%, CRM at 7.5%, NOW at 5.9%) are where the market already sits, so I avoid them (Exhibit 3).

Exhibit 3. Short interest as a share of float. The construction shorts the over-owned, low-short-interest longs and avoids the names the market is already short.

On valuation, I am candid about the limits of the short. Palantir is already down 26% year to date and 36% off its high, so this is not the act of shorting a euphoric top. The short rests on the absolute multiple, where 58 times sales remains extreme, on the August earnings event, and on the rate and duration channel. I enter on strength, with defined risk, rather than chasing momentum.

7. Macro backdrop: one pillar confirmed, one pending

The position rests on two macro conditions, and only one is present today. The rate pillar is confirmed: the June 17 FOMC meeting removed 2026 cuts, raised the median rate projection to 3.8%, and the incoming chair declined to submit a projection. The 10-year real yield sits at 2.19%, and the market prices roughly 15% odds of a December cut against 5% of a hike. The risk-off pillar is absent: the Institute for Supply Management (ISM) manufacturing index is near 54, the high-yield option-adjusted spread (OAS) is near 278 basis points (bp) at multi-decade tights, and the VIX is in the mid-teens. The oil and Hormuz reversal is disinflationary, which raises the odds of a soft inflation print.

I therefore run the position as a rate and duration trade with a gate, not a flight-to-safety bet. I hold a half-clip for the confirmed rate leg and scale to full weight only on a growth-deceleration signal: high-yield OAS above 350 bp, the ISM index below 50, payrolls below 100,000, or the VIX sustained above 22. The defined-risk structure is what allows a one-pillar regime to remain attractive: the loss is bounded, so the missing pillar is survivable rather than fatal.

8. Scenario analysis and expected return

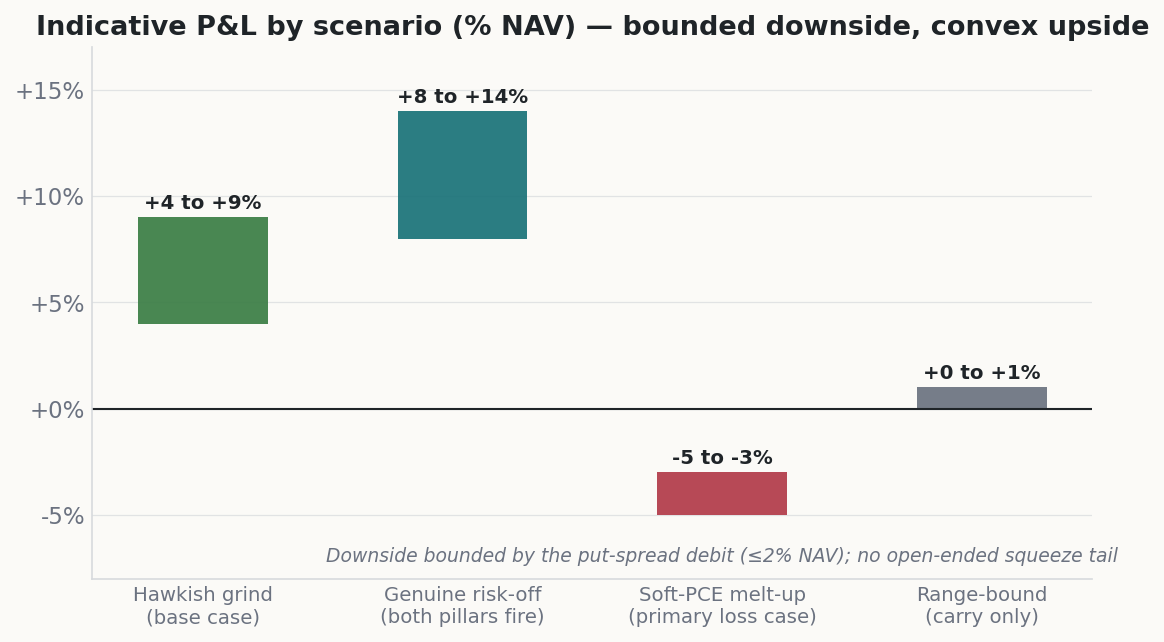

Carry is positive while the catalyst path develops. Net dividend carry runs 1.4% to 2.0% per annum on the cash long leg, and the short carries no borrow cost because it is expressed in options. The convexity is a one-time premium capped near 2% of NAV rather than a recurring drain. I model four scenarios over the horizon (Exhibit 4). The base case, a hawkish grind, returns 4% to 9% of NAV. A genuine risk-off returns 8% to 14%. A soft-print melt-up loses a bounded 3% to 5%. A range-bound tape pays the carry. The resulting reward-to-risk ratio exceeds 2.5 to 1, with the downside capped by the put-spread premium.

Exhibit 4. Indicative profit and loss by scenario. The melt-up loss is capped at the put-spread premium; there is no open-ended squeeze exposure.

The asymmetry is the case: a bounded 3% to 5% downside against 8% to 14% upside if the risk-off pillar confirms, and positive carry while waiting.

9. Implementation and sizing

I sequence entry in tranches, and entry can begin immediately because the loss is bounded:

| Step | Action |

|---|---|

| Pre-trade | Re-pull live betas, Palantir and Oracle short interest and borrow, option chains and implied volatilities, and the WCLD price near $29.3; drop any put spread that does not clear 2.5 to 1 |

| First tranche, about 50% | Buy XLP in full, SCHD at 60% with energy trimmed, IHF at 50% without chasing the one-year high; add the Palantir put spread into strength |

| After the May inflation print on June 25 | A hot core reading adds the Oracle and WCLD spreads and the final cash tranche; a soft reading halts adds, with the premium capping the loss |

| Full weight | Only after a growth-deceleration signal prints; until then I hold a half-clip and treat the book as a rate trade |

10. Catalysts and invalidation

The catalyst path is dated and one-directional if inflation stays sticky: the May inflation print on June 25, the July FOMC meeting alongside Microsoft earnings, the August labor and inflation prints, Palantir earnings in August, Oracle earnings on September 14, and the September FOMC meeting with updated projections. I close or cut on a confirmed thesis break rather than on noise:

| Condition | Action |

|---|---|

| Soft June 25 inflation print that re-prices 2026 cuts | Halt adds; cut the short overlay to the bounded premium |

| 10-year real yield below 1.85% | The rate leg is no longer supportive; reduce |

| Hormuz reopening, oil below $70, and dovish Fed commentary together | Revert to long-only |

| Long-versus-short ratio drawdown beyond 6% | Halve the position |

| Short cohort reclaims prior highs on a dovish pivot | Cover the spreads |

11. Risks to my view

The principal risk is regime: only the rate pillar is confirmed, and a soft inflation print or a dovish repricing would lift duration and software together, against both legs at once. The Oracle leg works only through the multiple-compression channel, since its cloud fundamentals are accelerating, so a re-rating on fundamentals rather than rates would not validate it. The Palantir short, already well off its high, depends on the absolute multiple and the August print rather than on fresh downside momentum. IHF concentrates 41% in two names, which carries single-stock event risk. Finally, the neutrality and reward-to-risk figures depend on betas and option pricing that I re-verify at execution; a materially different beta or a put-spread that does not clear my reward-to-risk threshold would reduce or remove that leg.

Disclosures

This document is produced for informational purposes only. It is not investment advice, nor an offer or solicitation to buy or sell any security or derivative. The analysis reflects my views as of June 18, 2026 and is subject to change without notice. Figures are drawn from a point-in-time research snapshot and have not been updated for subsequent market moves; the scenario analysis is hypothetical and is not a forecast or a guarantee of future results. Options carry the risk of total loss of premium. I may hold positions in the securities referenced. Readers should perform their own due diligence and consult a licensed adviser before acting.

Sources used: Federal Reserve June 17 statement, Federal Reserve H.15 selected interest rates, BEA personal income and outlays, ICE BofA U.S. High Yield option-adjusted spread (FRED), CME FedWatch, Schwab U.S. Dividend Equity ETF (SCHD), Oracle fourth-quarter fiscal 2026 results, Palantir investor relations, FINRA short interest.