Copper call spread: defined-risk HG upside

A 2-4 week HG copper options memo using a defined-risk call spread to express the tariff-premium and supply-risk thesis while capping downside at the debit.

I want HG copper exposure through options, with the risk defined by premium paid rather than by a live stop in the underlier. I'll go through institutional positioning, fundamentals, and macro in this post.

The clean expression is a 6.50/7.00 call spread in the first liquid monthly expiry that extends beyond the late-June U.S. copper tariff window.

| Item | Plan |

|---|---|

| Structure | Buy 6.50 call, sell 7.00 call |

| Expiry | First liquid monthly option that covers the late-June tariff decision |

| Preferred debit | 0.08-0.12 per lb |

| Maximum acceptable debit | Around 0.15 per lb |

| Thesis invalidation | Daily close below 6.15 or a broken tariff-premium catalyst |

Use Options

The thesis is bullish, but not clean enough for open-ended directional exposure. Copper has momentum, supply stress, and a live U.S. tariff catalyst. It also has crowded spec length, a refined-market surplus in the latest data, and demand evidence that is not yet strong enough to ignore.

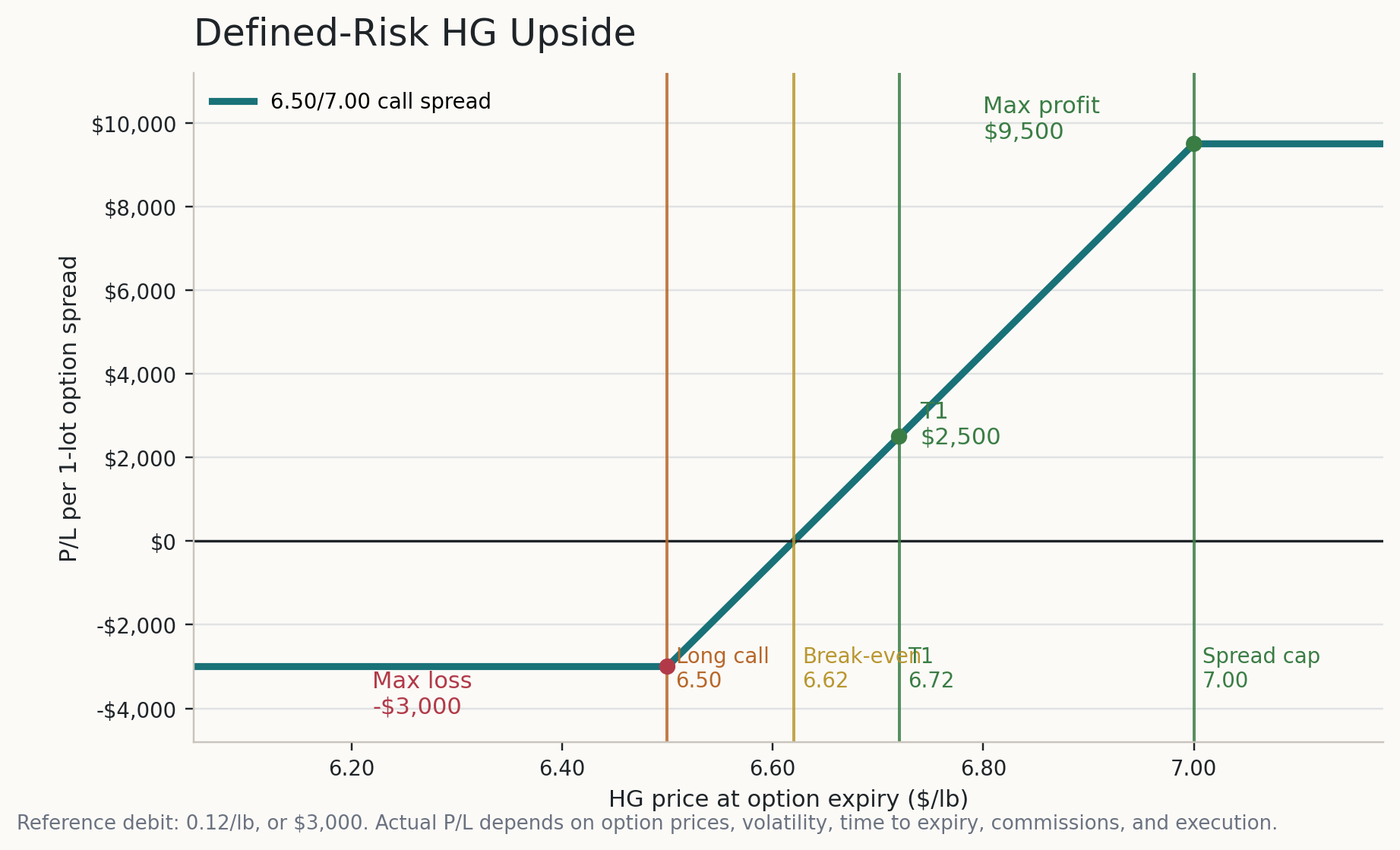

Payoff

At a 0.12 debit, the spread risks about $3,000 and breaks even at 6.62 at expiry. The first target at 6.72 is useful for de-risking. The real payoff comes from a push toward the short strike.

The spread is designed for a move into the target zone, not for unlimited upside exposure.

Reference expiry math:

| HG at expiry | Spread value | P/L at 0.12 debit | Read |

|---|---|---|---|

6.50 or lower | 0.00 | -$3,000 | Full premium loss |

6.62 | 0.12 | $0 | Break-even |

6.72 | 0.22 | +$2,500 | De-risking zone |

7.00 or higher | 0.50 | +$9,500 | Max profit zone |

That payoff shape is the point. The trade can be wrong without requiring a large mark-to-market drawdown. If copper does reach the target quickly, I should monetize the spread rather than admire it.

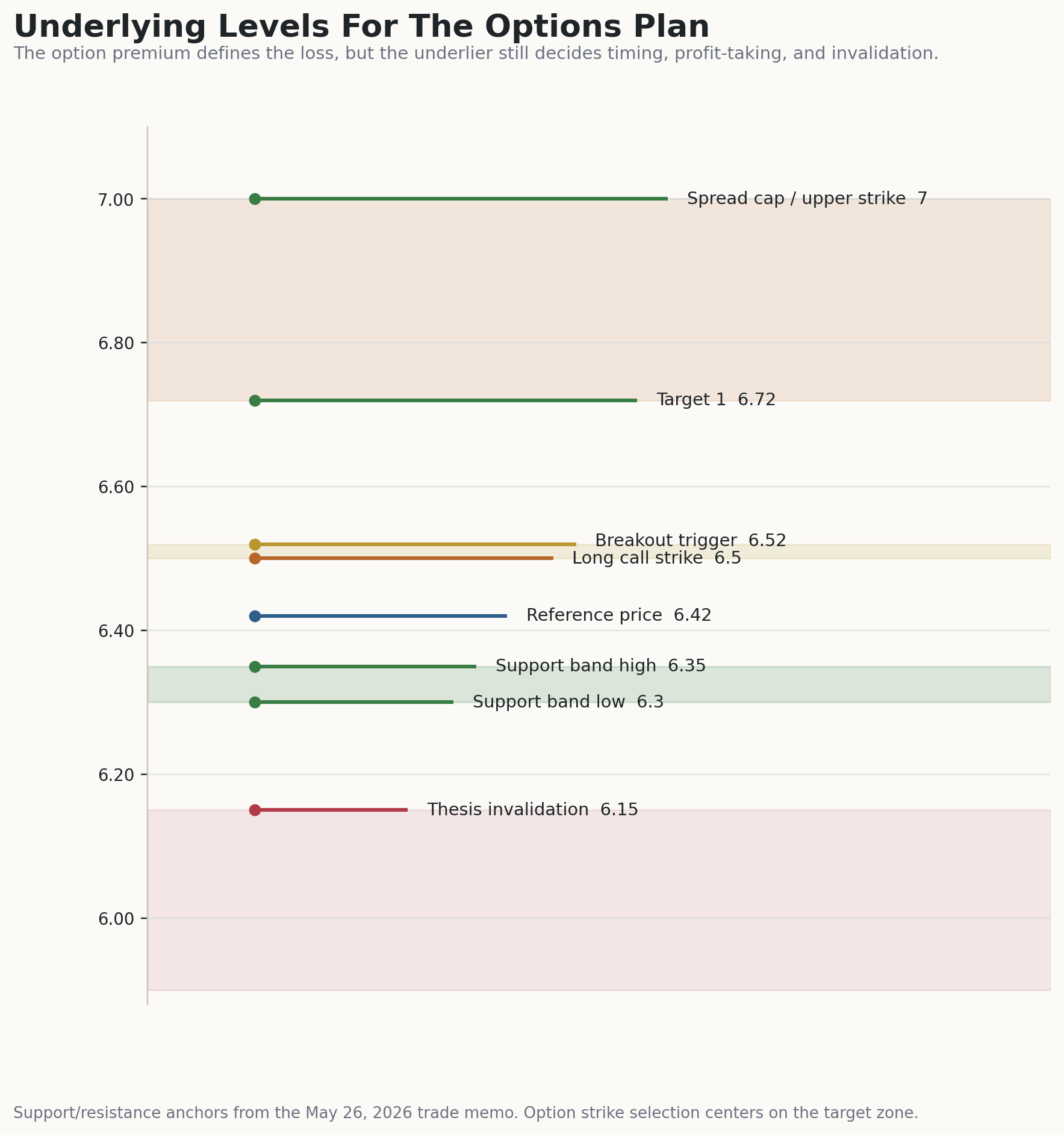

Underlying Map

The premium defines the loss, but the underlier still controls entry quality, timing, and invalidation.

The preferred entry is either a defended pullback into support or acceptance above the breakout trigger while the spread is still priced reasonably.

The levels that matter:

| Level | Role |

|---|---|

6.30-6.35 | Preferred pullback zone if buyers defend it |

6.50-6.52 | Long call strike and breakout trigger |

6.72 | First profit-management area |

7.00 | Short strike and main target |

6.15 | Thesis invalidation |

I prefer buying the spread after a controlled test of 6.30-6.35. A breakout entry above 6.52 is acceptable only if the spread remains inside the debit limit and the move has volume/open-interest confirmation.

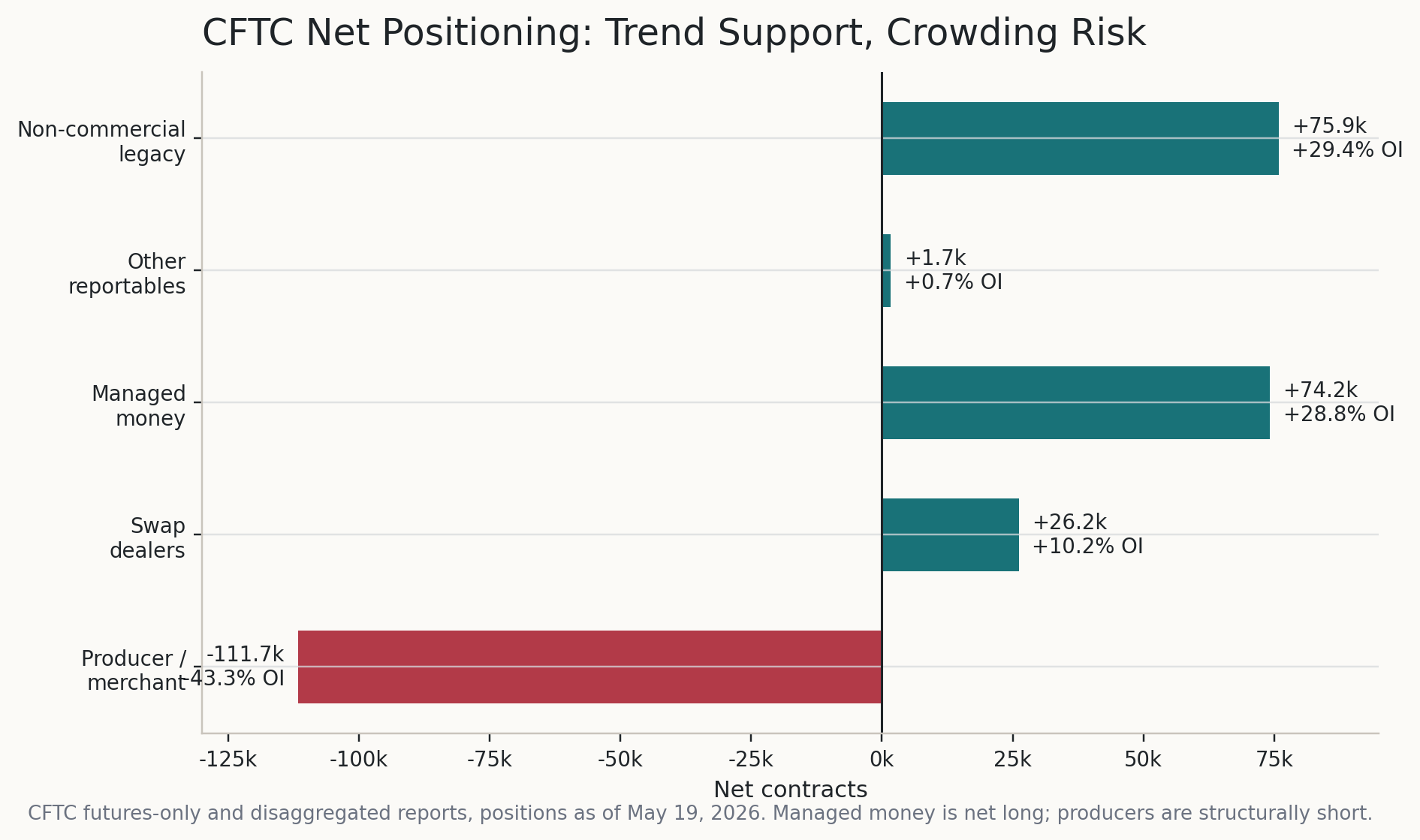

Positioning

Positioning supports the trend, but it is also the main reason to avoid an uncapped downside structure. The May 19 CFTC futures-only report showed non-commercials long 107,483 contracts and short 31,597, a net long of about 75.9k. The disaggregated report showed managed money long 87,457 and short 13,269, a net long of about 74.2k.

Long spec positioning confirms momentum, but the same crowd can become liquidation pressure if the breakout fails.

My read:

| Positioning fact | Bullish read | Risk read |

|---|---|---|

Managed money net long roughly 74.2k | Trend has sponsorship | Crowded longs can liquidate quickly |

Non-commercial net long roughly 75.9k | Speculative money is aligned with the move | A failed breakout can become a position unwind |

Producer/merchant net short roughly 111.7k | Hedging is normal at high prices | Commercial pressure is not a reason to chase |

Fundamentals

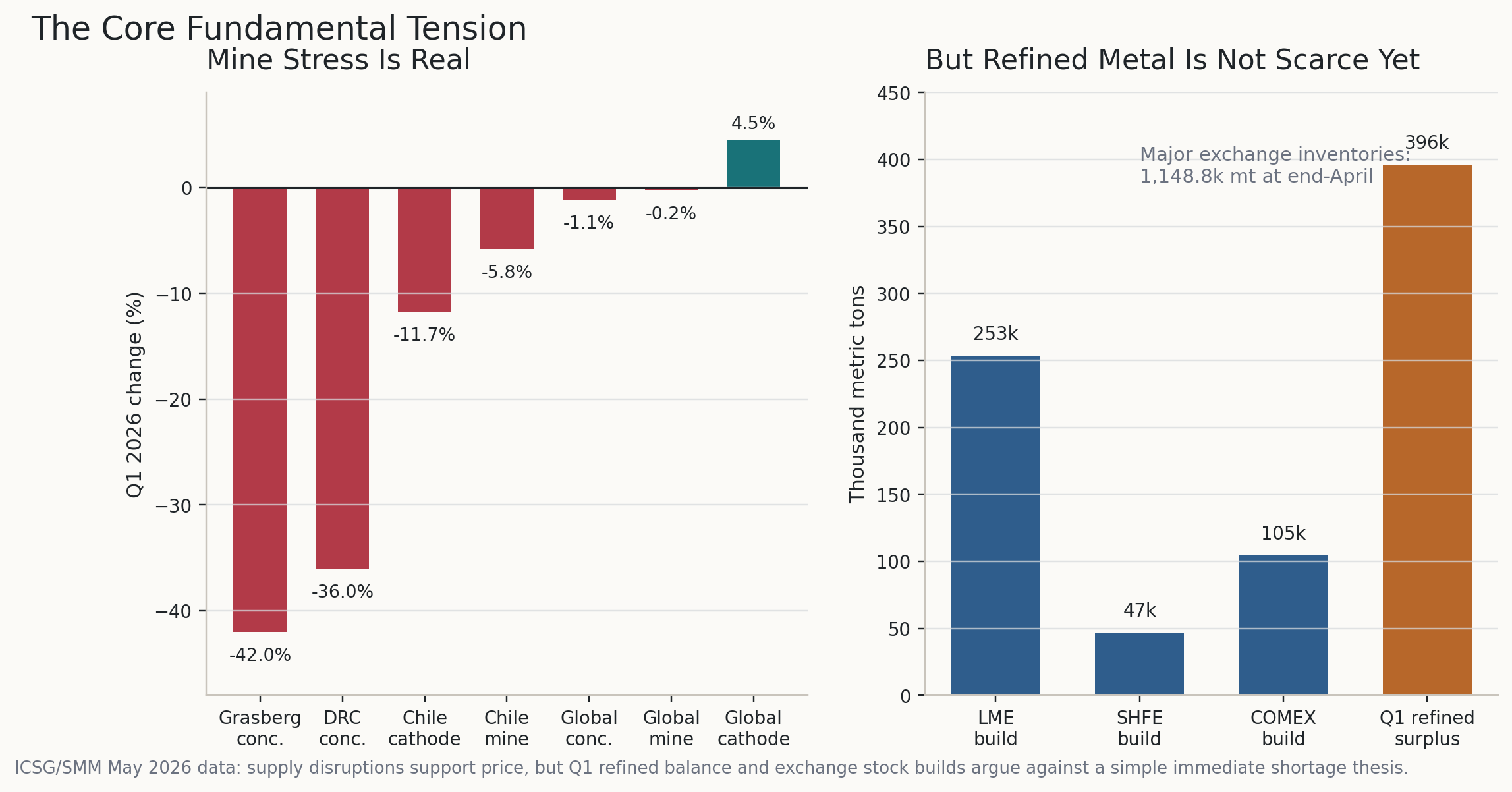

The fundamental story is supportive but not one-dimensional. Mine supply stress is real. The ICSG/SMM May data showed Q1 global mine production basically flat, copper concentrates down 1.1%, Grasberg concentrates down 42%, Chile mine production down 5.8%, and DRC concentrates down 36% because of Kamoa-related disruption. Chile cathode production also fell sharply.

The refined-market data are less supportive. The same ICSG/SMM update showed Q1 refined copper oversupply of about 396k mt, and major exchange inventories of 1,148.8k mt at the end of April, the highest level since January 2003. Exchange inventories had increased by about 404.6k mt since the end of 2025.

Supply risk supports upside optionality, but the inventory picture argues against treating the trade as a simple shortage story.

My conclusion: this is a supply-risk, tariff-premium, regional-tightness trade.

Macro Catalyst

The best catalyst is the U.S. copper tariff decision due by late June. Reuters reported that Trafigura planned to withdraw large amounts of copper from LME warehouses in New Orleans ahead of that ruling. Reuters also reported that cancelled LME copper stocks were nearly 30% of total LME stocks, while COMEX-approved warehouse stocks had risen to 574,864 mt, up more than 550% since the Section 232 investigation began.

That fits the option window. It explains why COMEX can stay firm even while the global refined balance looks loose. Metal has moved toward the U.S. because pre-tariff domestic supply has option value.

The risk is equally clear. If tariffs are delayed, diluted, or dismissed, the COMEX premium can compress. In that version, the spread can decay quickly even if the global copper story remains broadly constructive.

Demand Check

Demand is the main reason I do not want to overpay for the options. Reuters noted on May 22 that China demand was expected to taper as the country entered the seasonal off-season, and SHFE copper stocks rose for the first time since mid-March. ICSG/SMM also reported China's apparent demand was basically flat in Q1, with net copper cathode imports down 40%.

The signs I want:

| Confirmation | Why it matters |

|---|---|

| SHFE stocks resume drawing | Confirms Chinese absorption despite high price |

| China spot premiums improve | Shows real buyers, not only screen pressure |

| COMEX premium remains firm | Keeps the tariff/regional squeeze alive |

| LME available stocks keep tightening | Supports the stock-cancellation story |

Price holds 6.30-6.35 on a pullback | Confirms buyers defend the trend |

The trade can work without all of these, but the rating cannot move toward 9/10 unless demand stops contradicting the supply story.

Execution Plan

My execution rules:

| Trigger | Action |

|---|---|

Pullback into 6.30-6.35 and hold | Buy the 6.50/7.00 call spread if debit is near 0.08-0.12 |

Daily acceptance above 6.52 | Buy only if the spread is not above the debit limit |

Spread offered above 0.15 | Pass, wait, or redesign the strikes |

Daily close below 6.30 | Downgrade; reduce or exit if the spread has not held value |

Daily close below 6.15 | Thesis invalidated; exit remaining premium |

Trade into 6.72 | De-risk, take partial profit, or tighten exit rules |

Trade into 7.00 | Monetize the spread; capped upside has done its job |

Rating

| Version | Rating | Reason |

|---|---|---|

Spread debit above 0.15 | 6/10 | Good thesis, but too much premium for the risk mix |

Spread debit near 0.12 | 7/10 | Coherent defined-risk exposure with acceptable asymmetry |

Pullback holds 6.30-6.35 and spread cheapens | 8/10 | Better entry, lower break-even, cleaner invalidation |

| Pullback plus positioning reset and physical confirmation | 8.5-9/10 | Strong catalyst, better demand evidence, and cleaner option pricing |

The key is to treat premium as the position size. The spread is attractive only if I can buy convexity without paying so much that the market needs to be perfect.

Verdict

I like the copper upside thesis, but I want it expressed through a defined-risk option spread. The trade should pay if HG pushes into 6.72-7.00 during the tariff window, and the loss is capped if the crowded long trade unwinds.